A Gentle Intro to Support Vector Machines

Topics/Organization:

- Some geometric intuition for SVMs

- Introducing slack variables (Soft-Margin SVMs)

- The SVM loss function (primal and dual forms)

- SVMs and Kernels

- Some coding examples of the above (for fun!)

Some Geometric Intuition for SVMs

Support Vector Machines (SVMs) are a class of non-deep learning ML algorithm that can be used for both classification and regression problems. SVMs are extremelly powerful (we will see why!) and were considered top performing during early 1990s-2000s.

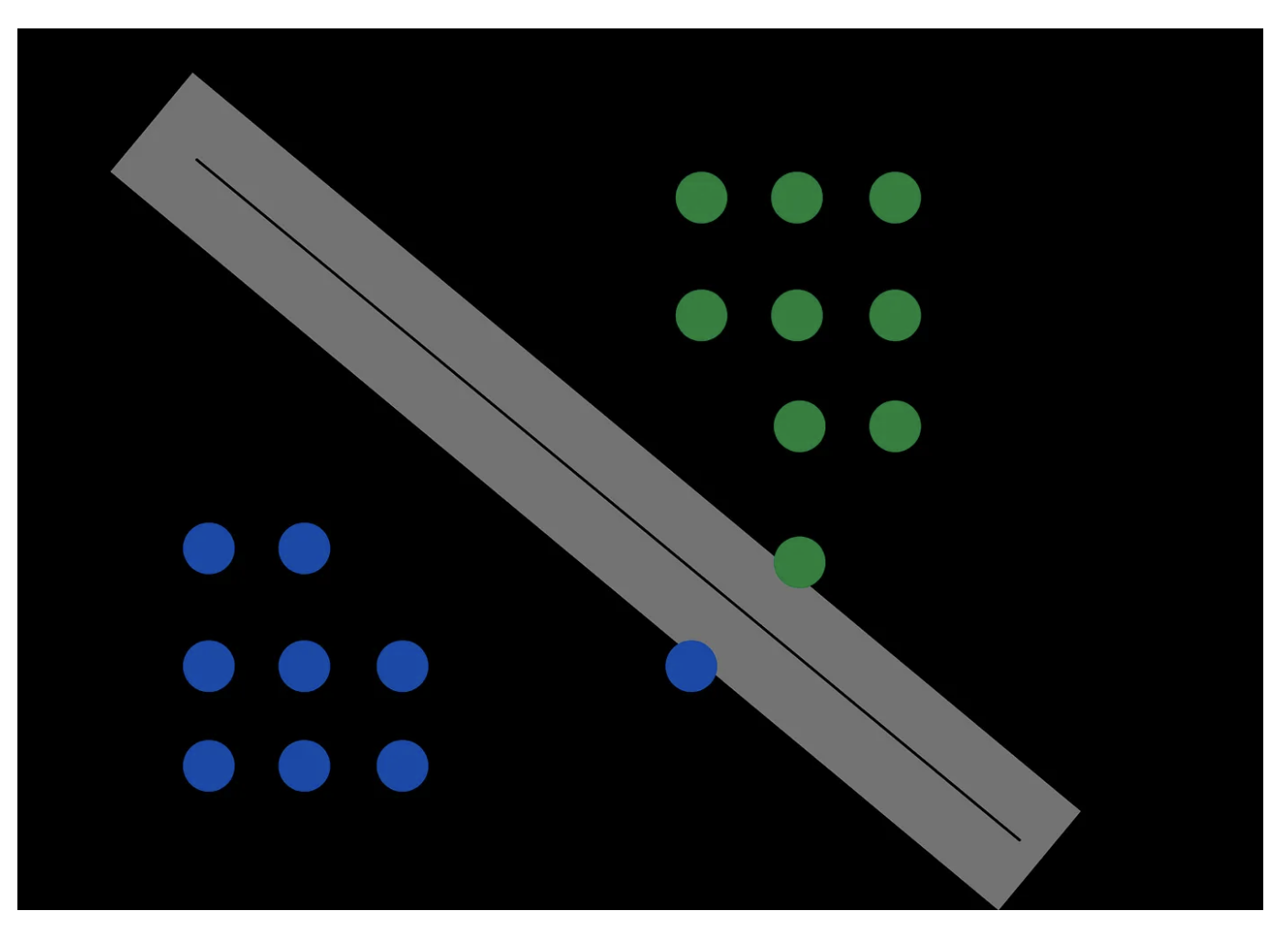

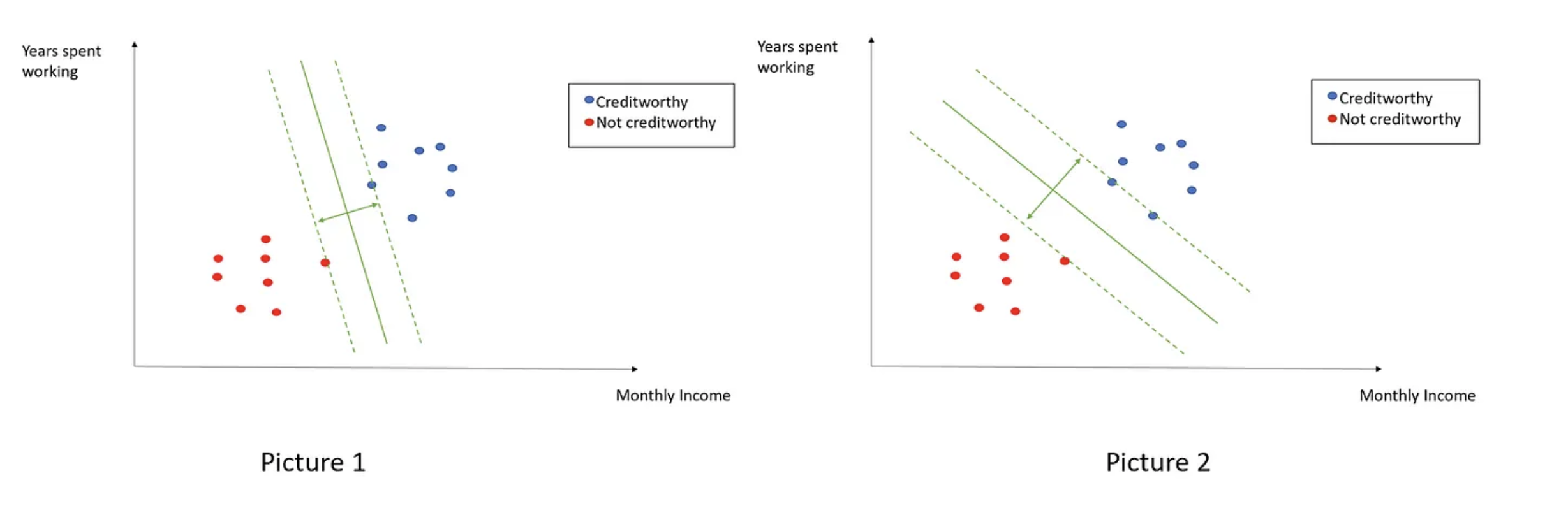

The main idea behind SVMs is that if we have some p-dimensional data (i.e., \(\mathbf{X} \in \mathbb{R}^p, \; Y \in \{1, -1\}\)), SVMs try to find the \(n-1\) dimensional hyperplane that best separates the two classes.

Best here is in the sense that this is the hyperplane that maximizes the margins (i.e., distances) between the closest points in the positive/negative classes and the decision boundary. That is why these models are often called wide margin classifiers.

But, why is maximizing these margins better?

- Avoid overfitting

- This reduces generalization error

Let’s illustrate the above with some schematics…

Ok, now let’s try to write this same intuition using some equations! Begin by considering the equations for the positive and negative (class) planes:

Now, subtract these two and divide result by the \(L_2\) norm of \(\mathbf{W}\):

Note that the LHS is essentially the distance between the positive and negative class hyperplanes, which is exactly what we said we wanted to maximize… Therefore, the optimization problem we are trying to solve is:

Note that, in the above the constraint \(Y_i(\mathbf{W^\top \cdot X_i} + b) \geq 1\) comes from the assumption that our data are linearly separable – this is the so-called Hard-margin SVM.

Soft-Margin SVMs and Slack variables

Well, but most real data out there are not linearly separable at all…. So, we need an SVM framework that can deal with these cases. To do so, let’s re-write the original SVM objective as follows:

Note that we swapped the original \(\text{argmax}\) problem for its corresponding \(\text{argmin}\) one and added an additional penalty/loss term \(C \frac{1}{n} \sum_{i=1}^n \xi_i\), where \(C\) is a tunnable hyper-parameter and \(\xi\) represents the distance of misclassified points from their actual/correct plane. Let’s look at an example here:

In the above, the distance between \(x_1\) and the plane \(\pi\) is 0.5 towards the negative plane. That is:

This shows that \(\xi\) is truly the distance of the misclassified point to its actual plane (in this case \(\pi^+\)). \(\xi\) is also known as a slack variable!

And the hyper-parameter \(C\) represents how strongly we penalize our model for violating our margins and misclassiying points. Therefore, as \(C\) increases, our model will tend to overfit the data, and vice-versa.

The SVM Loss

Primal Form

Looking at the Soft-Margin SVM objective, we can guess (intuitively) that we will want to minimize this distance of misclassified points from their true/correct plane (i.e., we wish to minimize our slack variable, \(\xi\)). In the case of SVMs, this is done through what we call a hinge loss mechanism. Let’s dive into it!

Starting with the last equation from above, we can write:

Now let \(Y(\mathbf{W^\top X} + b) = Z\) and note that if \(Z \geq 1\) then the point is correctly classified and, conversely, if \(Z < 1\), then the point is misclassified. Using this definition for \(Z\), we can re-write the above as:

Now, hinge losses are functions with the following property - their values are non-zero until a certain point after which they are equal to zero. SVMs optimize a hinge loss of the form:

Let’s see how this behaves… Well, if \(Z\geq1\) (i.e., pt is correctly classified), then \(\text{Max}(0, 1-Z) = 0\). That is, our loss is zero. On the other hand, if \(Z \leq 1\) (i.e., we misclassified pt) then \(\text{Max}(0, 1-Z) = 1-Z\). That is, we get some positive loss. Great, this is exactly what we want (look back at the Soft-Margin SVM objective again)!

Dual Form

Of note, the Soft-Margin SVM objective we’ve been discussing - \(\text{argmin}\left(\frac{\lVert \mathbf{W} \rVert}{2} \right) + C \frac{1}{n} \sum_{i=1}^n \xi_i\) - can be written in the following, mathematically equivalent form:

This is called the dual form and corresponds what’s called in convex optimization theory the dual problem. Proving that these are equivalent formally would require me to explain a good chunk of convex optimization theory and is quite involved – so I decided not to that today! But if you are curious about it, here are some excellent reads on it:

- Convex_Optim_Notes - these are Cynthia Rudin’s notes on topic (awesome, but technically dense!)

- Deriving_SVM_Dual - also from Cynthia Rudin. Explains/derives above dual form in detail for SVMs.

- YouTube Lecture SVMs - starting at 30mins, when he derives dual form.

SVMs and Kernels

Well, the reason I bothered showing you the dual form above is because it helps us see why SVMs are considered to be kernel based methods and is what makes them so powerful. But before we dive into that, a couple of points …

What is a kernel?

Kernel can mean many different things in math, BUT here we are specifically considering Mercer Kernels, that is, symmetric positive definite kernels.

More specifically, a Mercer kernel is any symmetric function \(\mathcal{K} : \mathcal{X} \times \mathcal{X} \to \mathbb{R}^{+}\), s.t.:

with equality iff \(c_i=0 \, \forall i\). Put it another way, if I give you \(N\) data points and a Mercer kernel \(\mathcal{K}(., .)\), we can defined a Gram matrix:

which has to be symmetric and positive definite for any set of distinct inputs. There are many, many times of Mercer kernels - for a quick reference on these, check out the kernel_cookbook.

Some (popular) examples of valid kernels

- Linear Kernel \(k(x,y) = x^Ty\)

- Polynomial Kernel \(k(x,y) = (\gamma x^Ty + c_0)^d\)

- d is the polynomial degree

- RBF Kernel \(k(x,y) = \exp({\frac{-\lVert x - y \rVert^2}{2\sigma^2}})\)

- Called Gaussian if \(y = \bar{x}\)

- \(\sigma\) influences tightness of fit, as you can imagine, a low \(\sigma\) will induce overfitting

How can we construct valid kernels from existing ones?

This is NOT an exhaustive list btw!

- \(k(x,x') = ck_1(x,x')\), where \(c > 0\) is a constant and \(k_1(x,x')\) is a known valid kernel

- \(k(x,x') = f(x)k_1(x,x')f(x')\) where \(f\) is any function

- \(k(x,x') = q(k_1(x,x'))\) where \(q\) is a polynomial with nonnegative coefficients

- \(k(x,x') = \exp(k_1(x,x'))\).

- \(k(x,x') = k_1(x,x') + k_2(x,x')\) where \(k_1\) and \(k_2\) are both known valid kernels

- \(k(x,x') = k_1(x,x')k_2(x,x')\).

- \(k(x,x') = x^TAx\), where \(A\) is a symmetric positive semidefinite matrix

The Kernel Trick

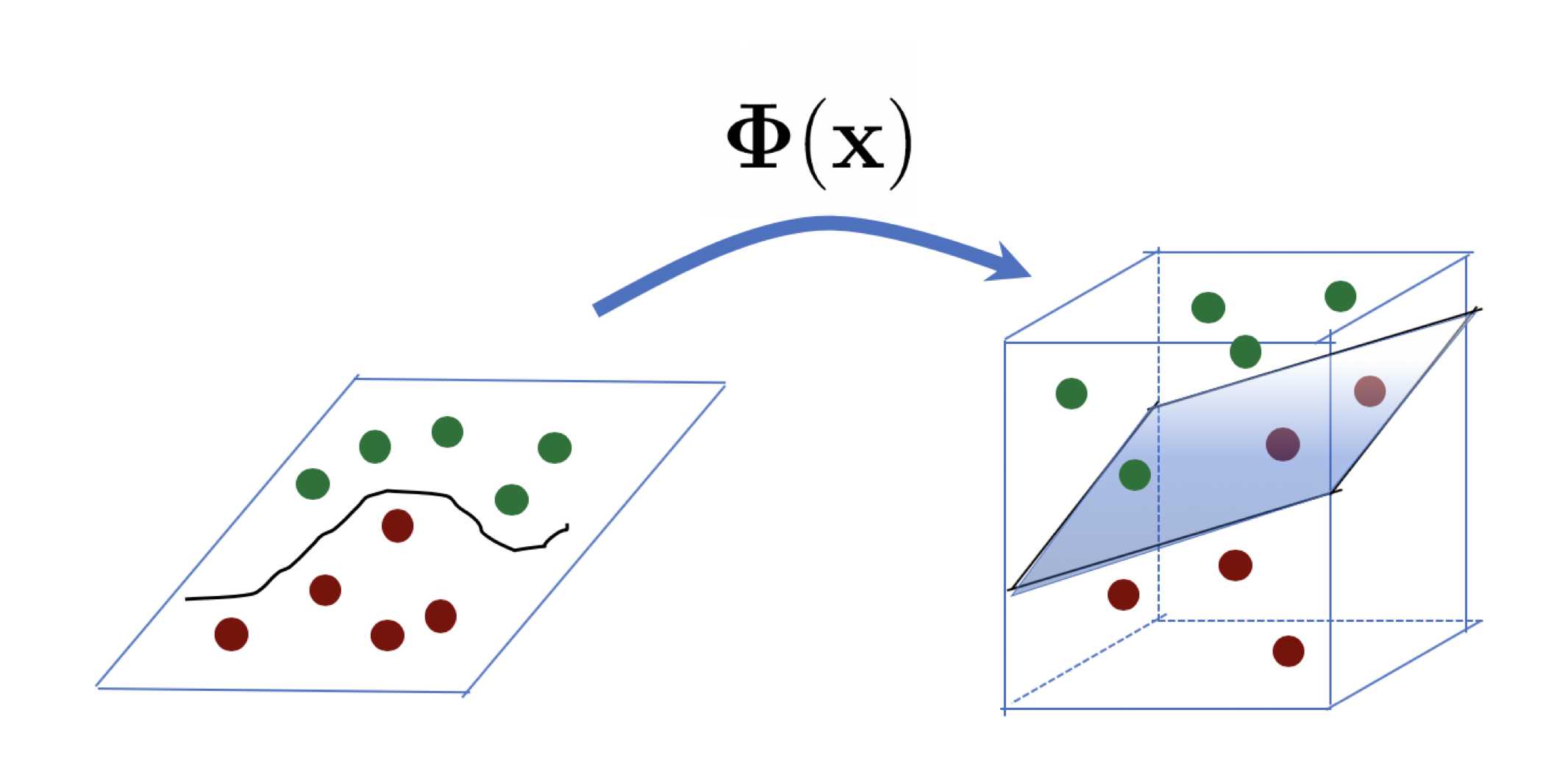

Oftentimes, we wish to work with datasets that aren’t linearly seperable in one dimensional space, so it can be helpful to use a mapping function \(\Phi(x)\) to a higher dimensional space where the data are linearly separable. This trategy is known as the kernel trick. The mathematical details of why this is true are beyond the scope of this presentation, but they related to the so-called Mercer’s theorem. If you are curious about it, Kevin Murphy’s Probabilistic ML book offers a great explanation on it!

- Murphy’s Probabilistic ML Book, check chapter 18 - prob_ML_book

Tying it all back

In the dual form I presented before \(\text{Max} \left\{ \sum_{i=1}^n \alpha_i - \frac{1}{2} \sum_{i=1}^n \sum_{j=1}^n \alpha_i \alpha_j y_i y_j x_i^\top x_j \right \}\) , note that we are taking the inner(i.e.,dot) product of \(x_i\) and \(x_j\). We can replace this inner product by a valid kernel (which preserves inner products!) and all else works as desired! That is, we can more generally write:

where \(K(x_i, x_j)\) is any valid Mercer Kernel. That is, we can apply the kernel trick here to be able to separate our data better, even if it is not linearly separable (in its ambient/original dimensional space).

Coding Examples

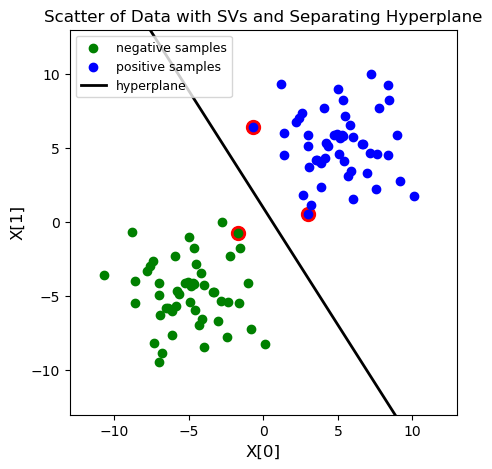

Let’s look at a linearly separable case first. For this, am working with some toy data generared as follows:

- \(X_{neg} \sim \mathcal{N}([-5, -5], 5*I_2)\) and correspond to negative labels (-1)

- \(X_{pos} \sim \mathcal{N}([5, 5], 5*I_2)\) and correspond to positive labels (+1)

Then, I use libsvm (an existing implementation of SVMs)to fit an SVM to these data and highlight our supporting vectors (SVs).

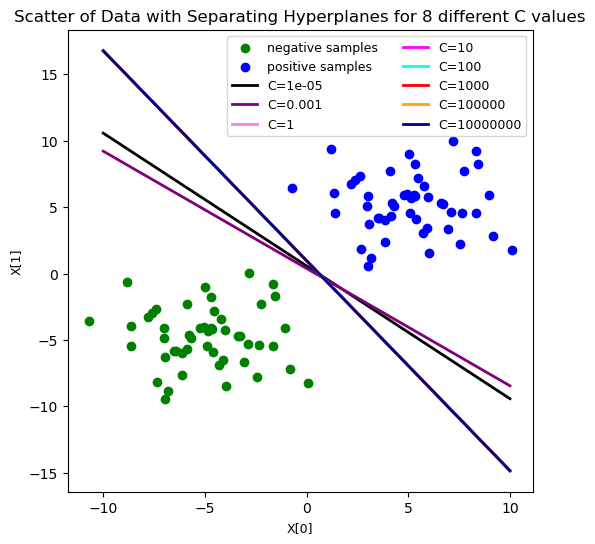

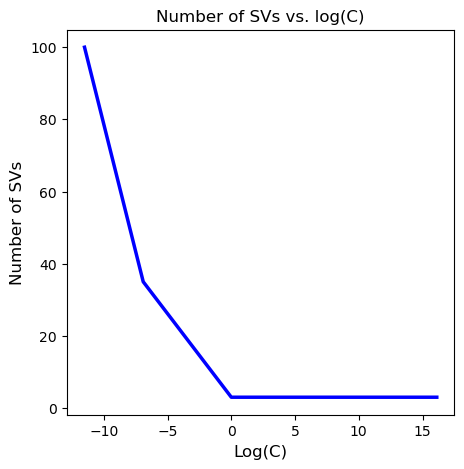

Finally, I vary the value of the hyperparameter \(C\) and plot the different decision boundaries achieved, as well as the number of SVs by C vals (in log scale).

1

2

3

4

5

6

7

8

9

import numpy as np

import matplotlib.pyplot as plt

import scipy.io as io

import libsvm

from libsvm.svmutil import *

from scipy.stats import multivariate_normal

from sklearn.model_selection import train_test_split

%matplotlib inline

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

#gen data

X_neg = multivariate_normal.rvs(mean=[-5, -5], cov=(5*np.eye(2)), \

size=50, random_state=np.random.seed(0))

X_pos = multivariate_normal.rvs(mean=[5, 5], cov=(5*np.eye(2)), \

size=50, random_state=np.random.seed(0))

X = np.concatenate([X_neg, X_pos], axis=0)

neg_labels = np.repeat(-1, 50)

pos_labels = np.repeat(1, 50)

Y = np.concatenate([neg_labels, pos_labels], axis=0)

#set up our SVM problem and train

prob = svm_problem(Y, X)

options = svm_parameter('-s 0 -t 0') #linear kernel, C type

model = svm_train(prob, options)

#Compute the slope and intercept of the separating line/hyperplanee

w = np.matmul(X[np.array(model.get_sv_indices()) - 1].T, model.get_sv_coef())

b = -model.rho.contents.value

#report slope and intercept vals

print('*'*40)

print('Slope of the hyperplane is :')

print(w)

print('Intercept of hyperplane is:')

print(b)

print('*'*40)

# Draw the scatter plot, the decision boundary line, and mark the support vectors.

plt.figure(figsize=(5,5))

for i in model.get_sv_indices():

plt.scatter(X[i - 1][0], X[i - 1][1], color='red', s=100)

plt.scatter(X[:50, 0], X[:50, 1], color='green', label='negative samples')

plt.scatter(X[50:, 0], X[50:, 1], color='blue', label='positive samples')

plt.plot([-10, 10], [-(-10 * w[0] + b) / w[1], -(10 * w[0] + b) / w[1]], color='black', \

linewidth=2, label='hyperplane')

plt.xlim([-13, 13])

plt.ylim([-13, 13])

plt.title('Scatter of Data with SVs and Separating Hyperplane', fontsize=12)

plt.xlabel('X[0]', fontsize=12)

plt.ylabel('X[1]', fontsize=12)

plt.legend(loc='upper left', fontsize=9)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

*****************************************

optimization finished, #iter = 10

Slope of the hyperplane is :

[[0.36172799]

[0.22875099]]

Intercept of hyperplane is:

-0.22133232278883996

****************************************

nu = 0.001832

obj = -0.091576, rho = 0.221332

nSV = 3, nBSV = 0

Total nSV = 3

<matplotlib.legend.Legend at 0x7fcd99e9b7d0>

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

#now let's play around with our C hyper-param value

C_range = [10**-5, 10**-3, 1, 10, 100, 10**3, 10**5, 10**7]

num_sv = []

ws = []

bs = []

for c in C_range:

prob = svm_problem(Y, X)

options = svm_parameter('-s 0 -t 0 -c {} -q'.format(c)) #linear kernel, C type, C==c

model = svm_train(prob, options)

w = np.matmul(X[np.array(model.get_sv_indices()) - 1].T, model.get_sv_coef())

b = -model.rho.contents.value

ws.append(w)

bs.append(b)

num_sv.append(len(model.get_sv_indices()))

num_sv = np.array(num_sv)

ws = np.array(ws)

bs = np.array(bs)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

#plot the decision boundaries for the difference C vals

plt.figure(figsize=(6, 6))

colors = ['black', 'purple', 'violet', 'magenta', 'cyan', 'red', 'orange', 'darkblue']

plt.scatter(X[:50, 0], X[:50, 1], color='green', label='negative samples')

plt.scatter(X[50:, 0], X[50:, 1], color='blue', label='positive samples')

for i in range(len(C_range)):

plt.plot([-10, 10], [-(-10 * ws[i][0] + bs[i]) / ws[i][1], -(10 * ws[i][0] +\

bs[i]) / ws[i][1]], \

color=colors[i], linewidth=2, label='C={}'.format(C_range[i]))

plt.title('Scatter of Data with Separating Hyperplanes for 8 different C values', \

fontsize=12)

plt.xlabel('X[0]', fontsize=9)

plt.ylabel('X[1]', fontsize=9)

plt.legend(loc='best', ncol=2, fontsize=9)

1

<matplotlib.legend.Legend at 0x7fcdf9b62310>

1

2

3

4

5

6

#now plot the #SVs by log(C)

plt.figure(figsize=(5,5))

plt.plot(np.log(C_range), num_sv, color='blue', linewidth=2.5)

plt.title('Number of SVs vs. log(C)', fontsize=12)

plt.xlabel('Log(C)', fontsize=12)

plt.ylabel('Number of SVs', fontsize=12)

1

Text(0, 0.5, 'Number of SVs')

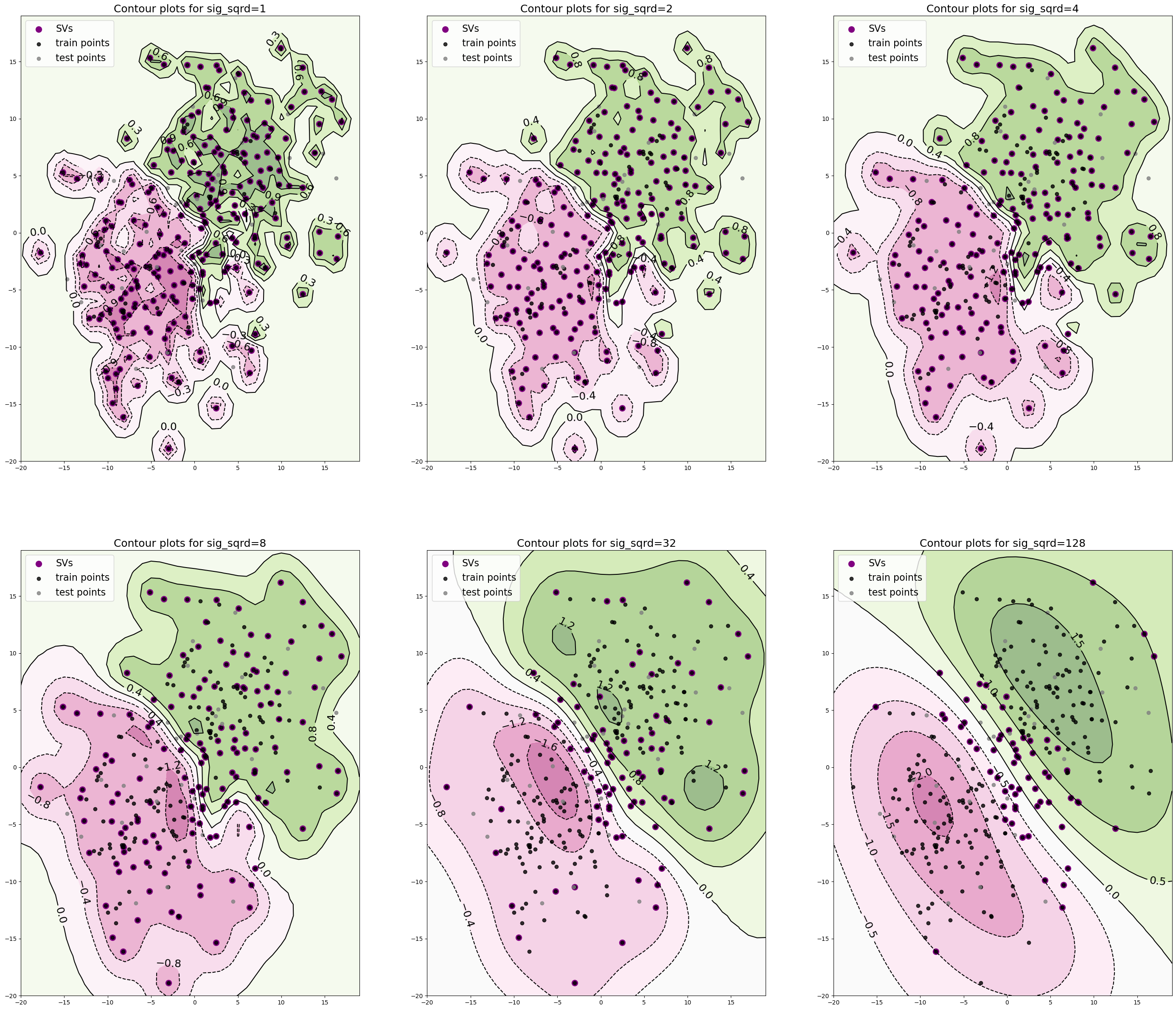

Now, let’s look at a non-linearly separable case and play around with kernels! We start similarly, generating some toy data as follows:

• \(X_{neg} ∼ N([-5, -5], 25·I_2)\) and corresponds to negative labels (−1)

• \(X_{pos} ∼ N([5, 5], 25·I_2)\) and corresponds to positive labels (+1)

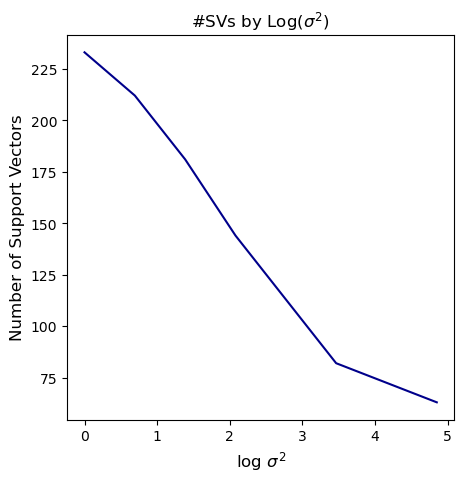

And, once again, we use libsvm (only with different settings) to fit an SVM to these data and construct contour plots for the decision function f and explicitly plot the decision boundary as well. Finally, let’s look at how these countour plots as well as the number of SVs change as we vary the \(\sigma^2\) in our kernel.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

#gen data

X_neg = multivariate_normal.rvs(mean=[-5, -5], cov=(25*np.eye(2)), \

size=150, random_state=np.random.seed(0))

X_pos = multivariate_normal.rvs(mean=[5, 5], cov=(25*np.eye(2)), \

size=150, random_state=np.random.seed(0))

X = np.concatenate([X_neg, X_pos], axis=0)

neg_labels = np.repeat(-1, 150)

pos_labels = np.repeat(1, 150)

Y = np.concatenate([neg_labels, pos_labels], axis=0)

#split it into train/test

X_tr, X_te, y_tr, y_te = train_test_split(X, Y, test_size=0.10, random_state=5)

#fit model (with \gamma = 1/\sigma^2 = 1/25)

prob = svm_problem(y_tr, X_tr)

options = svm_parameter('-s 0 -t 2 -g 0.04 -q') #Gaussian kernel, C type, gamma=1/25

model = svm_train(prob, options)

#Get SVs

SVs = X_tr[np.array(model.get_sv_indices()) - 1]

#prep stuff we need for 2D contour plots

x_min, x_max = -20, 20

y_min, y_max = -20, 20

xx, yy = np.meshgrid(np.arange(x_min, x_max, 1),

np.arange(y_min, y_max, 1))

Z = []

for i in range(xx.shape[0]):

curr_z_row = []

for j in range(yy.shape[0]):

item = np.array([xx[i, j], yy[i,j]])

item = np.expand_dims(item, axis=0)

z_ij = svm_predict([], item, model, '-q')

curr_z_row.append(z_ij[2][0])

Z.append(np.array(curr_z_row))

Z = np.squeeze(np.array(Z))

#construct plots

plt.figure(figsize=(6, 6))

plt.contourf(xx, yy, Z, cmap=plt.cm.PiYG, alpha=0.5)

CS = plt.contour(xx, yy, Z, colors='black')

plt.clabel(CS, inline=1, fontsize=10)

plt.scatter(SVs[:, 0], SVs[:, 1], color='violet', label='SVs', s=80)

plt.scatter(X_tr[:, 0], X_tr[:, 1], color='black', alpha = 0.8, label='train points')

plt.scatter(X_te[:, 0], X_te[:, 1], color='gray', alpha = 0.8,label='test points')

plt.legend(loc='best')

#report train/test set accuracies

pred_tr = svm_predict(y_tr, X_tr, model, '-q')

tr_acc = pred_tr[1][0]

pred_te = svm_predict(y_te, X_te, model, '-q')

te_acc = pred_te[1][0]

print('*'*40)

print('Train accuracy is: {:.3f}'.format(tr_acc))

print('Test accuracy is: {:.3f}'.format(te_acc))

print('*'*40)

1

2

3

4

****************************************

Train accuracy is: 93.704

Test accuracy is: 90.000

****************************************

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

#now fit same data using rbf kernel SVM with varying sigmas

#code here could be var more efifcient/pretty

#will clean it up before uploading final version of all materials to website

#gen sig_sqrds, gammas

sig_sqrds = [1, 2, 4, 8, 32, 128]

gammas = [1/i for i in sig_sqrds]

#def small func to get our Z vals

def get_Zs(xx, yy, model):

"""

Constructs 2D Z array to be passed onto contour and contourf for

constructing the desired plots.

Args:

xx: 2D arr output from meshgrid

yy: 2D arr output from meshgrid

model: LIBSVM model -- especified using an SVM problem and a set

of param options.

"""

Z = []

for i in range(xx.shape[0]):

curr_z_row = []

for j in range(yy.shape[0]):

item = np.array([xx[i, j], yy[i,j]])

item = np.expand_dims(item, axis=0)

z_ij = svm_predict([], item, model, '-q')

curr_z_row.append(z_ij[2][0])

Z.append(np.array(curr_z_row))

Z = np.squeeze(np.array(Z))

return Z

#train/fit models and collect all vars we want

tr_acc = []

te_acc = []

SVs = []

nsvs = []

Zs = []

for g in gammas:

prob = svm_problem(y_tr, X_tr)

options = svm_parameter('-s 0 -t 2 -g {} -q'.format(g))

model = svm_train(prob, options)

nsvs.append(len(model.get_sv_indices()))

SVs.append(X_tr[np.array(model.get_sv_indices()) - 1])

pred_tr = svm_predict(y_tr, X_tr, model, '-q')

tr_acc.append(pred_tr[1][0])

pred_te = svm_predict(y_te, X_te, model, '-q')

te_acc.append(pred_te[1][0])

curr_Z = get_Zs(xx, yy, model)

Zs.append(curr_Z)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

#now construct contourplots, report accuracies

#construct #SVs by \sigma^2 plot.

def construct_countour_plots(xx, yy, Zs, SVs, X_tr, X_te, sigmas):

"""

Constructs a (2,3) plot mat containing results of above

model fittings using 6 different vals for \sigma^2

Args

----

xx: 2D arr output from meshgrid

yy: 2D arr output from meshgrid

Zs: list containing level set info for plotting.

SVs: list containing SVs for each sim.

X_tr: np.arr containing train data

X_te: np.arr containg test data

sigmas: options of sigma^2 values tested

"""

fig, axs = plt.subplots(2,3, figsize=(35, 30))

for i in range(2):

for j in range(3):

idx = i*3 + j

sig = sigmas[idx]

axs[i, j].contourf(xx, yy, Zs[idx], cmap=plt.cm.PiYG, alpha=0.5)

CS = axs[i, j].contour(xx, yy, Zs[idx], colors='black')

plt.clabel(CS, inline=1, fontsize=18)

axs[i, j].scatter(SVs[idx][:, 0], SVs[idx][:, 1], \

color='purple', label='SVs', s=100)

axs[i, j].scatter(X_tr[:, 0], X_tr[:, 1], color='black',\

alpha = 0.8, label='train points')

axs[i, j].scatter(X_te[:, 0], X_te[:, 1], color='gray', \

alpha = 0.8,label='test points')

axs[i, j].legend(loc='best', fontsize=16)

axs[i, j].set_title('Contour plots for sig_sqrd={}'.format(sig), \

fontsize=18)

return

1

construct_countour_plots(xx, yy, Zs, SVs, X_tr, X_te, sig_sqrds)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

#now report accuracies

#and plot #SVs by sig

for s in range(len(sig_sqrds)):

print('*'*40)

print('Train/Test Accuracies for Sig_Sqrd = {}'.format(sig_sqrds[s]))

print('Train set accuracy:{:.4f}'.format(tr_acc[s]))

print('Test set accuracy:{:.4f}'.format(te_acc[s]))

print('*'*40)

plt.figure(figsize=(5, 5))

plt.plot(np.log(sig_sqrds), nsvs, color='darkblue')

plt.xlabel('log $$\sigma^2$$', fontsize=12)

plt.ylabel('Number of Support Vectors', fontsize=12)

plt.title('#SVs by Log($$\sigma^2$$)', fontsize=12)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

****************************************

Train/Test Accuracies for Sig_Sqrd = 1

Train set accuracy:97.4074

Test set accuracy:86.6667

****************************************

****************************************

Train/Test Accuracies for Sig_Sqrd = 2

Train set accuracy:96.2963

Test set accuracy:86.6667

****************************************

****************************************

Train/Test Accuracies for Sig_Sqrd = 4

Train set accuracy:95.1852

Test set accuracy:90.0000

****************************************

****************************************

Train/Test Accuracies for Sig_Sqrd = 8

Train set accuracy:94.4444

Test set accuracy:93.3333

****************************************

****************************************

Train/Test Accuracies for Sig_Sqrd = 32

Train set accuracy:93.7037

Test set accuracy:90.0000

****************************************

****************************************

Train/Test Accuracies for Sig_Sqrd = 128

Train set accuracy:93.3333

Test set accuracy:90.0000

****************************************

Text(0.5, 1.0, '#SVs by Log($$\\sigma^2$$)')